Here’s the short answer: neither public money nor private capital can do this alone. Public funds cover early science and production methods, research centres, and first-stage buildout. Private investors step in later, but only when they can see a route to sales, lower costs, and market demand.

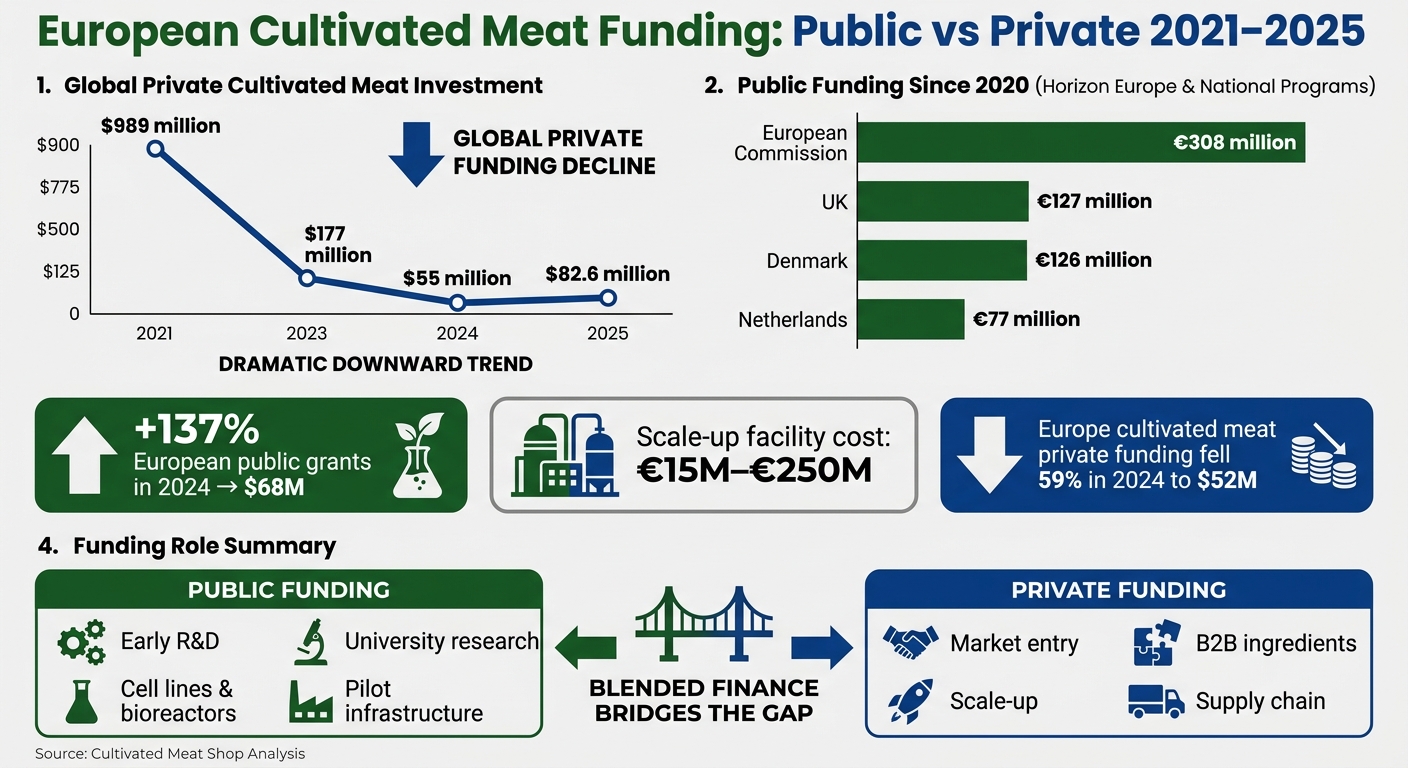

Right now, that split is getting sharper. Global private funding fell from $989 million in 2021 to $177 million in 2023, then to $55 million in 2024. At the same time, European public grants for alternative protein firms climbed 137% in 2024 to $68 million. That tells me one thing: the state is filling part of the gap while investors wait for proof.

If you want the article in one glance, it comes down to this:

- Public funding backs early R&D, university work, cell lines, media work, and pilot support

- Private funding backs firms closer to market, with clearer revenue plans

- The main problem is scale-up, where facilities can cost €15 million to €250 million

- The most likely route is blended finance: grants, public loans, and private money used together

- For Europe and the UK, this is tied to food supply, local production, and future industry buildout

European Cultivated Meat Funding: Public vs Private 2021–2025

Quick Comparison

| Funding type | Best for | Main strength | Main limit |

|---|---|---|---|

| Public funding | Early research, shared infrastructure, first-stage projects | Can back long timelines and high technical risk | Often slow and too small for full factory costs |

| Private funding | Market entry, scale-up, supply chain firms | Moves fast when the business case is clear | Harder to secure without proof of sales and cost control |

My take: public money starts the work, private money tests whether the business stands up, and blended finance is the only clear path to full production in Europe. This transition is detailed in our roadmap for cultivated meat.

sbb-itb-c323ed3

1. Public Funding

Public funding is paying for the long, expensive groundwork that private capital often sidesteps. Since 2020, the European Commission has put €308 million into alternative protein research and innovation through Horizon Europe and the European Innovation Council (EIC). The UK has invested €127 million, followed by Denmark at €126 million and the Netherlands at €77 million.[5]

Stage of Support

This money usually comes in at the earliest point. It backs university research, cell line development, bioreactor designs, and media optimisation, where the science is hard, the timeline is long, and investor appetite can be thin. The EU's FEASTS project is one example. It received public funding to assess how Cultivated Meat and seafood could fit into future food systems. At the applied end, the UK's National Alternative Protein Innovation Centre (NAPIC) launched with £16 million from BBSRC and Innovate UK to help bridge research and commercialisation.[1]

Once that base is in place, the focus shifts from lab work to the tougher job of building capacity.

Risk and Time Horizon

Public funding can sit with long development cycles in a way private money often can't. Robert Jones, VP Global Public Affairs at Mosa Meat, put it plainly:

"We need to be talking about this in terms of decades, not the next three, four or five years." [4]

That matters because public bodies can take on early-stage risk and are more often treating Cultivated Meat as an issue tied to food security and competitiveness.[4]

Infrastructure and Scale-Up

Scale-up is where costs start to bite. A demonstration or commercial-scale facility in Europe costs €15 million to €250 million, which puts it out of reach for most startups.[3] In 2022, the Dutch government set aside €60 million for a national Cultivated Meat and precision fermentation ecosystem. Then, in 2024, the EIC backed Infinite Roots' $58 million round.[3][5]

Regulatory and Market Impact

Public grants are also helping startups get ready for market entry. In 2025, Dutch startup Meatable secured $8.4 million from the Netherlands Enterprise Agency to support commercialisation work.[3] In 2024, Poland awarded a €2 million grant to LabFarm for Cultivated Meat R&D.[1]

Even with that early backing, private capital still has to step in if these companies are going to scale.

2. Private Funding

If public grants take the edge off early scientific risk, private capital tends to step in when it's time to show the business can work. That money played a big part in Cultivated Meat's early growth, but the mood has changed fast. Global private funding hit $989 million in 2021, then dropped to $177 million in 2023, $55 million in 2024, and edged back up to $82.6 million in 2025 [2]. In Europe, cultivated meat firms brought in $52 million (£48 million) in 2024, down 59% from the year before [3].

Stage of Support

Venture capital poured into the sector during the 2020–21 hype cycle. Now it's far more selective. Investors are backing firms that can show clearer unit economics, paid partnerships, and a path to revenue. Money is also moving towards companies that supply bioreactors, software, and growth media.

As Steven Finn, General Partner at Siddhi Capital, put it:

"Regulatory approvals are no longer fundable milestones. Now we need to see a real instance of a product coming into the market and working." [2]

Risk and Time Horizon

That shift pulls private investors towards models that can pay off sooner, especially B2B ingredients and blended products. Tighter capital has also pushed the sector towards consolidation. Instead of paying for new facilities, some better-funded players are buying infrastructure from weaker rivals.

Infrastructure and Scale-Up

Private capital has helped bring production costs down. UK-based Meatly used private investment to cut growth media costs from £700 per litre to £1 per litre [4]. In the UK, Multus opened a commercial-scale, serum-free culture media facility with private funding to tackle a major supply chain bottleneck [1]. Right now, private capital looks strongest when it comes to de-risking later-stage scale-up, rather than backing first-of-a-kind plants.

Regulatory and Market Impact

At this point, investors care less about approvals on their own and more about proof that customers are there. They want signs of demand, not just a green light from regulators. In April 2024, Mosa Meat raised $43 million in a round backed by strategic and private investors as it prepared for market entry [6].

Political risk is also weighing on sentiment. Bans in Italy and Hungary have made some investors more cautious about the size of Europe's market [1][6].

That split between early public risk-taking and later private discipline sets up the trade-offs below.

Pros and Cons of Each Funding Model

Neither funding model works well on its own. Public funding moves more slowly, but it can stay patient. Private capital moves faster, but now it wants stronger proof before writing a cheque. That difference shows up pretty clearly in practice:

| Public Funding | Private Funding (VC/PE) | |

|---|---|---|

| Primary goal | Food security, climate targets, ecosystem stability | High growth, rapid scaling, path to profitability |

| Best suited for | Long-term R&D, large-scale infrastructure, demo facilities | Early-stage innovation, B2B ingredients, market entry |

| Risk tolerance | High for technical, long-horizon projects | Lower than before; now demands commercial proof |

| Speed | Slower; tied to grant cycles and political priorities | Faster, but highly sensitive to market sentiment |

| Key weakness | Slower disbursement and often too small relative to total CapEx needs | Not suited to funding first-of-a-kind commercial facilities [1] |

The split is simple: public money helps absorb early risk, while private capital wants a clearer case that the business can sell, scale and make money.

The biggest pressure point is scale-up infrastructure and technical challenges. Building a demo or commercial-scale facility for alternative proteins can cost between €15 million and €250 million [3]. That’s well above what most public grants cover, and it’s also beyond what many private investors are willing to back when the plant is first-of-a-kind.

That funding gap is pushing more attention towards blended finance. In plain English, that means combining public support with private capital. The European Investment Bank’s €35 million venture loan to Formo in 2025 is a good example [3]. When public backing shows long-term commitment, it can give private investors enough confidence to step in rather than stay on the sidelines.

Conclusion

Across Europe, the pattern is clear: public money takes on the early risk, while private capital steps in once there’s proof the business can work.

Public funding helps de-risk early R&D and shared infrastructure. Private capital then supports scale-up and market entry. That split is what turns pilot plants into products that can, in time, reach shop shelves.

Blended finance - combining grants, concessional loans, and guarantees with private capital - is the most realistic way to bridge the gap between early-stage science and commercial production.

That matters because the speed of funding shapes when Cultivated Meat reaches consumers and how fast costs come down. For consumer-focused updates on Cultivated Meat, visit Cultivated Meat Shop.

FAQs

Why has private funding dropped so sharply?

Private funding for Cultivated Meat has dropped as the early buzz has worn off. After a stretch of cheap capital and strong investor appetite, backers have become more careful about companies that can’t show clear commercial viability or a believable path to profit.

At the same time, money has shifted into other fast-growing sectors. And venture capital often isn’t a good fit for the high cost of building first-of-a-kind production facilities.

What does blended finance mean in practice?

In practice, blended finance brings together public or philanthropic capital and private investment. The goal is simple: make it easier to fund sectors like Cultivated Meat, where projects can be new, expensive, and harder for private investors to back on their own.

This kind of public support can also work as a multiplier. It can help unlock more private funding and send a clear signal that there’s long-term confidence in the sector.

What is stopping Cultivated Meat from scaling faster in Europe?

Cultivated Meat in Europe is running into a big funding gap.

Private venture capital has dropped sharply. At the same time, public research and innovation funding still doesn't cover the high cost of producing cultivated meat at commercial scale.

Regulation is another drag on progress. Approvals often take more than two and a half years, which puts investors off and leads some start-ups to move abroad.